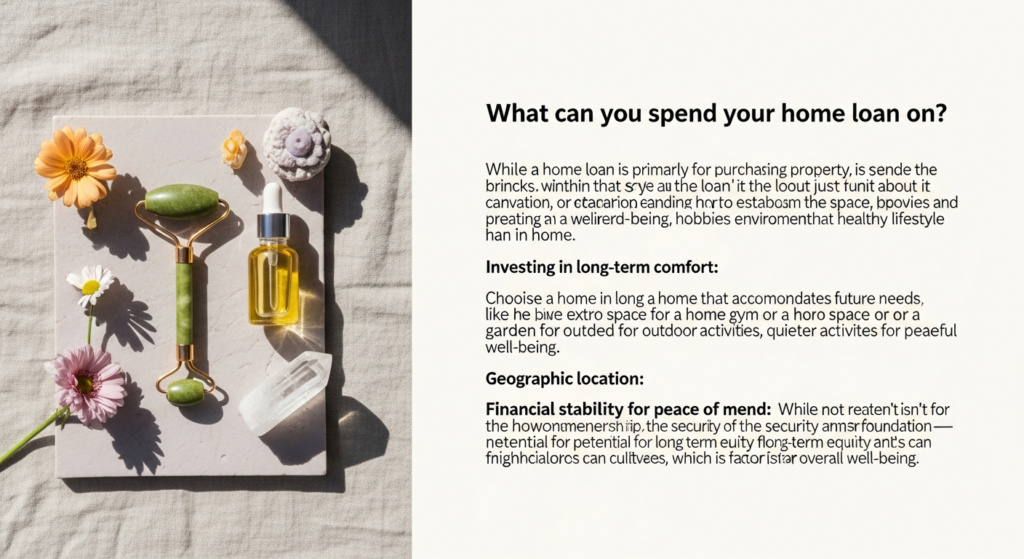

Understanding Your Home Loan: The Basics

Before diving into the specifics of spending, it’s essential to grasp the fundamental nature of a home loan. At its core, a home loan, often referred to as a mortgage, is a sum of money borrowed from a financial institution to purchase or maintain a home. This loan is secured by the property itself, meaning the lender can take possession of your home if you fail to repay the loan as agreed. While the primary purpose is home ownership, the equity you build in your home over time can become a powerful financial tool, accessible through various loan products.

There are several types of home-related financing options, each serving a distinct purpose:

- Purchase Mortgage: This is the most common type, used to buy a new home. It covers the majority of the home’s price, with the borrower typically providing a down payment.

- Refinance Mortgage: This involves replacing your existing mortgage with a new one. Reasons for refinancing include securing a lower interest rate, changing the loan term, or converting an adjustable-rate mortgage (ARM) to a fixed-rate mortgage.

- Cash-Out Refinance: A specific type of refinance where you take out a new mortgage for more than you currently owe on your home, receiving the difference in cash. This allows you to tap into your home equity.

- Home Equity Line of Credit (HELOC): A revolving line of credit secured by your home equity. It functions much like a credit card, allowing you to borrow, repay, and re-borrow funds up to a certain limit over a draw period.

- Home Equity Loan: Also known as a second mortgage, this provides a lump sum of money, secured by your home equity, with a fixed interest rate and repayment schedule.

Eligibility for any of these loans in 2026 hinges on several factors, including your credit score, debt-to-income (DTI) ratio, income stability, and the amount of equity you have in your home (for equity-based loans). Lenders assess these to determine your capacity to repay the loan, ensuring responsible lending practices and protecting both you and the financial institution.

Financing Your Dream Home Purchase

The most straightforward and common use of a home loan is, of course, to purchase a primary residence. This involves more than just the sticker price of the house; your home loan helps cover a myriad of expenses associated with acquiring property. Understanding these components is vital for accurate budgeting and avoiding unwelcome surprises as you embark on your homeownership journey in 2026.

- The Purchase Price: The bulk of your home loan will go towards paying the seller for the property itself. Your down payment covers a portion, and your mortgage finances the rest.

- Closing Costs: These are fees paid at the closing of a real estate transaction. They can range from 2% to 5% of the loan amount and often include:

- Loan Origination Fees: What the lender charges for processing your loan.

- Appraisal Fees: To determine the fair market value of the home.

- Inspection Fees: To assess the home’s condition and identify any potential issues.

- Title Insurance: Protects both the lender and you from future claims against the property’s title.

- Escrow Fees: Paid to the third party who holds funds and documents until the transaction is complete.

- Recording Fees: For officially recording the sale with local government.

- Prepaid Expenses: Often included in closing costs, these are items that must be paid in advance, such as property taxes and homeowner’s insurance premiums for a certain period. Lenders typically require an escrow account to hold funds for these ongoing costs (PITI – Principal, Interest, Taxes, Insurance).

When considering a new home purchase, whether it’s an existing property or new construction, your home loan facilitates the entire process. For new construction, the loan structure might differ slightly, sometimes involving construction loans that convert into traditional mortgages upon completion. Always factor in potential overages or delays when building. For existing homes, a thorough inspection is crucial to understand potential future expenses, which might influence your loan amount or your negotiation strategy.

Practical Tip: While your loan covers many costs, always budget for additional items like moving expenses, immediate repairs or upgrades, and furnishing your new home. Having a financial cushion beyond your loan amount ensures a smoother transition into your dream home.

Unlocking Equity: Refinancing and Cash-Out Options

Rate-and-Term Refinance: This type of refinance involves replacing your current mortgage with a new one, primarily to change the interest rate or the loan term. While it doesn’t provide cash directly, it can free up monthly cash flow by lowering your interest rate or extending your repayment period. Conversely, shortening your loan term can help you pay off your home faster, saving you a substantial amount in interest over the life of the loan. This can be a smart move for those nearing retirement, as reducing monthly housing costs or eliminating mortgage payments altogether provides significant financial freedom, aligning with sound financial planning for adjusting to retirement from handling finances to staying on top of your health.

Cash-Out Refinance: A cash-out refinance allows you to borrow against your home equity, receiving a lump sum of cash at closing. You take out a new mortgage that is larger than your current outstanding balance, and the difference is given to you in cash. This is a popular option for funding major expenses or consolidating debt due to typically lower interest rates compared to personal loans or credit cards.

Home Equity Line of Credit (HELOC): A HELOC functions like a credit card, providing a revolving line of credit secured by your home. You can draw funds as needed up to a pre-approved limit during a “draw period” (often 10 years), making interest payments only on the amount you’ve borrowed. After the draw period, you enter a “repayment period” where you pay back the principal and interest. HELOCs offer flexibility for ongoing expenses or projects that evolve over time.

Home Equity Loan: Unlike a HELOC, a home equity loan provides a lump sum of cash upfront, which you repay over a fixed term with a fixed interest rate. It’s often chosen for specific, one-time large expenses where you know the exact amount you need.

Considerations: While unlocking equity offers significant benefits, remember that these loans use your home as collateral. Defaulting on a cash-out refinance, HELOC, or home equity loan could lead to foreclosure. Always weigh the benefits against the risks and ensure you have a solid repayment plan.

Transforming Your Space: Home Renovations and Improvements

One of the most popular and often financially savvy uses of a home loan is to fund renovations and home improvements. Whether you’re dreaming of a gourmet kitchen, an expanded living space, or energy-efficient upgrades, leveraging your home equity can make these projects a reality. In 2026, homeowners continue to invest in their properties, not just for personal enjoyment but also to enhance market value and prepare for future resale.

You can finance renovations through several home loan mechanisms:

- Cash-Out Refinance: As discussed, this provides a lump sum that can be fully dedicated to your renovation project. It’s suitable for large, well-defined projects.

- HELOC: Ideal for phased renovations or projects where costs might fluctuate. You can draw funds as needed for different stages of the project, paying interest only on what you’ve used.

- Home Equity Loan: A good choice for a single, significant renovation project with a clear budget, as it provides a fixed amount with predictable payments.

- Construction Loans: For major structural changes or additions, a specific construction loan might be necessary. These are short-term loans that convert to a permanent mortgage upon project completion.

Types of renovations that home loans commonly cover include:

- Kitchen and Bathroom Remodels: These often yield the highest return on investment (ROI) and significantly enhance daily living.

- Room Additions: Expanding your home’s footprint with new bedrooms, bathrooms, or living areas.

- Basement Finishing: Converting an unfinished basement into usable living space.

- Energy-Efficient Upgrades: Installing solar panels, new windows, or high-efficiency HVAC systems can reduce utility bills and increase home value.

- Exterior Improvements: Landscaping, new roofing, siding, or deck additions.

When planning renovations, it’s crucial to heed critical home renovation dos and don’ts. Do set a realistic budget and stick to it, obtain multiple quotes from licensed contractors, and understand local building codes. Don’t start without a clear plan, over-customize to the point of alienating future buyers, or neglect proper permits. A well-planned renovation not only improves your quality of life but can also significantly boost your home’s appraisal value, making it a sound financial investment for the long term.

Strategic Financial Moves: Debt Consolidation and Investment

Beyond home improvements, a home loan can be a powerful instrument for strategic financial planning. Many homeowners in 2026 are leveraging their home equity to consolidate high-interest debt or make smart investments, thereby improving their overall financial health and long-term wealth accumulation.

Debt Consolidation

If you’re burdened by high-interest debt such as credit card balances, personal loans, or even student loans, a cash-out refinance or home equity loan can offer a lifeline. By consolidating these debts into a single home loan, you can often achieve:

- Lower Interest Rates: Home loans typically have significantly lower interest rates than unsecured debts, leading to substantial savings over time.

- Simplified Payments: Instead of juggling multiple monthly payments, you’ll have one predictable payment.

- Improved Cash Flow: Lower monthly payments can free up cash, making your budget more manageable.

While the benefits are clear, it’s crucial to understand the risks. You are converting unsecured debt into secured debt, meaning your home is now collateral. If you default on your consolidated home loan, you risk foreclosure. This strategy requires discipline to avoid accumulating new high-interest debt after consolidation. It’s a tool for getting out of debt, not for enabling more spending. For those nearing retirement, consolidating debt can be a crucial step in adjusting to retirement from handling finances to staying on top of your health, ensuring a more secure and less stressful financial future.

Investment Opportunities

A home loan can also be used to fund various investment ventures:

- Rental Properties: Using a cash-out refinance or a home equity loan to fund the down payment or purchase of an investment property can generate passive income and build wealth through real estate appreciation.

- Major Life Purchases: While not a traditional “investment,” using a home loan for a significant, planned purchase that enhances your lifestyle or provides long-term value can be a wise move. For instance, some families might use a HELOC to fund a substantial part of an RV purchase, enabling them to take family RV road trips and create lasting memories without depleting other savings. This can be viewed as an investment in family experiences and well-being.

- Business Ventures: Entrepreneurs sometimes use home equity to inject capital into a new or existing business, leveraging lower interest rates to fuel growth.

- Education: As discussed in the next section, investing in higher education for yourself or your children can be a valuable long-term investment.

Each investment carries its own risk, and it’s imperative to conduct thorough research and potentially consult with a financial advisor before committing your home equity to such ventures. The goal is to ensure that the potential returns or benefits outweigh the risks associated with borrowing against your primary asset.

Beyond the Bricks: Other Permitted Uses

The versatility of home equity extends beyond renovations and direct financial restructuring. In 2026, homeowners are increasingly using their home loans for a variety of significant personal expenses, leveraging the lower interest rates and tax advantages that these financial products can offer compared to other forms of credit.

Education Expenses

Funding higher education, whether for yourself or your children, is a common and often wise use of home equity. College tuition, room and board, and other educational costs can be substantial. A cash-out refinance, HELOC, or home equity loan can provide the necessary funds, often at a lower interest rate than private student loans or personal loans. This can significantly reduce the overall cost of education and make repayment more manageable. It’s an investment in human capital that can yield substantial returns over a lifetime.

Medical Emergencies and Healthcare Costs

Life is unpredictable, and unexpected medical emergencies can lead to significant out-of-pocket expenses, even with good health insurance. When faced with large medical bills, a home equity loan or HELOC can provide a much-needed financial safety net. Accessing funds through your home loan can help cover surgeries, extensive treatments, or long-term care needs, preventing you from incurring high-interest credit card debt during a stressful time. This can be particularly relevant for those adjusting to retirement from handling finances to staying on top of your health, as healthcare costs often increase with age.

Large Personal Purchases

While discretion is advised, a home loan can be used to finance other significant personal purchases that might otherwise be out of reach or require high-interest financing. This could include:

- Vehicle Purchases: Buying a new car, truck, or even an RV for family adventures. For instance, using a portion of a HELOC to fund a substantial down payment or the entire cost of an RV could enable those tips for taking a family RV road trip you’ve always dreamed of, creating invaluable experiences. The key is to ensure the interest rate on the home loan is significantly lower than a traditional auto loan.

- Wedding Expenses: For couples planning a large wedding, a home equity loan could cover costs, though careful consideration of the long-term debt implications is essential.

- Travel and Vacations: While generally not recommended for discretionary spending, in specific circumstances, a HELOC might fund a once-in-a-lifetime trip, especially if other savings are tied up or not sufficient. However, it’s crucial to prioritize needs over wants when borrowing against your home.

The critical question for any “beyond the bricks” expenditure is: Is this a wise use of my home equity? Leveraging your home for discretionary spending carries risk. Always consider the long-term financial implications, the interest you’ll pay, and whether the purchase truly justifies putting your home on the line. Prudent financial planning means making informed choices that enhance your life without jeopardizing your most valuable asset.

Making Smart Decisions: Planning and Pitfalls

While a home loan offers incredible flexibility and financial power, making smart decisions is paramount. In 2026, navigating the complexities of borrowing requires careful planning, a clear understanding of the terms, and an awareness of potential pitfalls. The goal is always to enhance your financial well-being, not to undermine it.

Comprehensive Financial Planning

Before you commit to any home loan product, engage in thorough financial planning. This includes:

- Budgeting: Understand your current income and expenses. Can you comfortably afford the new monthly payments, including principal, interest, taxes, and insurance (PITI)? Factor in potential interest rate increases if you’re considering an adjustable-rate product like a HELOC.

- Goal Setting: Clearly define what you want to achieve with the funds. Is it a necessary renovation, debt consolidation, or a major investment? Having a clear goal helps you choose the right loan product and prevents impulse borrowing.

- Emergency Fund: Ensure you have a robust emergency fund separate from your home equity. Tapping into your home equity for emergencies should be a last resort, not a primary strategy.

Understanding Interest Rates and Terms

The devil is often in the details. Pay close attention to:

- Interest Rates: Compare rates from multiple lenders. Understand if the rate is fixed or variable, and how a variable rate might impact your payments over time.

- Fees: Beyond interest, home loans come with various fees (origination, appraisal, closing costs). Factor these into your total cost of borrowing.

- Repayment Schedule: Know your monthly payment amount, the total number of payments, and the overall cost of the loan.

- Prepayment Penalties: Some loans have penalties for paying off the loan early. Be aware of these if you plan to accelerate repayment.

Risks and Pitfalls to Avoid

- Over-borrowing: Just because you can borrow a certain amount doesn’t mean you should. Borrow only what you need and can comfortably repay. Over-leveraging your home puts your primary asset at risk.

- Using Home Equity for Frivolous Spending: While a HELOC offers flexibility, using it for non-essential, depreciating assets or impulse purchases is generally ill-advised. Your home is collateral, and you don’t want to risk it for short-term gratification.

- Ignoring Market Conditions: If you’re planning a cash-out refinance for renovations, consider the current housing market. Will the renovation add value that you can recoup if you sell in the near future?

- Not Shopping Around: Different lenders offer different rates and terms. Always get quotes from several financial institutions to ensure you’re getting the best deal.

- Falling for Scams: Be wary of unsolicited offers or lenders promising deals that seem too good to be true. Always verify credentials and work with reputable institutions.

Seeking Professional Advice: Before making any significant financial decision involving your home loan, consider consulting with a financial advisor or a mortgage specialist. They can help you assess your individual situation, understand the implications of different loan products, and create a plan that supports your long-term financial health. For women navigating retirement, this is especially crucial, as sound financial advice can help tailor strategies for adjusting to retirement from handling finances to staying on top of your health, ensuring a secure and comfortable future.

Frequently Asked Questions

Recommended Resources

Check out How To Find Your Personal Style As A Woman on Sometimes Daily for a deeper dive.

Learn more about this topic in Best Tinted Moisturizer 2026 Comparison at Fashion Goggled.